Here we will create a depth guide About blockchain technology. So choose wisely to achieve the ultimate goal through high-level Performance.

Blockchain Explained

A question arises in mind: what is blockchain technology? It is a peer-to-peer ledger system that lets people trade with each other without having to go through a central authority.

We know that anyone who does not run a peer-to-peer network. Peers each have their copy of the ledger, so it’s not all run by one person. In This case, the catalog can be a complete copy or just the parts needed to keep it connected to the network.

Consensus methods like Proof-of-Work, Proof-of-Stake, or others ensure that all transactions are the same. Advanced cryptographic algorithms also make sure that each transaction is safe. So it’s clear that the whole blockchain system takes advantage of trust, immutability, and transparency, which are all good things. People don’t like the idea of centralization.

It is a network of people who can make transactions without a single person. Right now, This simple idea is completely changing how businesses work.

History Of Blockchain

A blockchain is a digital ledger that isn’t owned or controlled by anyone. It stores data lists—a cryptographic method to put these lists into safe blocks and arrange them in chronological order. In 2009, bitcoin hit the market, and many people thought of the invention of blockchain.

This work led others to think of new ways to use cryptography and look for new jobs in the field. When these computer scientists did their work, bitcoin was born. It was the first wholly decentralized and permissionless digital cash platform. It led to a wide range of Blockchain technology and projects today.

Key Feature Of Blockchain

These things make blockchain technology different from other types of technology.

Instead of putting a single person in charge, blockchain uses a network of users to validate and keep track of transactions. Because of It, transactions on the blockchain are always the same, fast, safe, affordable, and tamper-proof. These traits are below:

- There is no need for one or more people to act as middlemen.

- In this case. Blockchain networks worldwide work 24 hours a day, seven days a week.

- Blockchain networks are less expensive to run because they don’t have centralized, rent-seeking intermediaries that charge fees.

- Secure: A blockchain’s network of nodes protects each other from attacks and outages.

- Once time-stamped to the ledger, making the blockchain resistant to fraud and other crimes. With a public blockchain network, everyone can see the transactions.

Type Of Blockchain

It is possible to use a blockchain network in different ways. A blockchain network can in many different ways, and there are many ways to do it. They can be public, private, or built by a consortium group.

1. Public blockchain network:

A public blockchain is anyone can look at, send transactions to, and expect those transactions if they are valid and part of the consensus process, which decides which blocks to the chain and what the current state is. This process is called consensus.

Bitcoin and Ethereum use crypto-economics to keep their public blockchains safe. It is because crypt economics combines economic incentives with cryptographic verification using procedures like proof of work (Bitcoin) or proof of stake (Ethereum). In general, these blockchains are “completely decentralized.”

Public blockchains are a way to protect app users from their developers. They show that some actions are beyond even the app’s developers’ control. Many businesses will use public blockchains because they are open and don’t need to be checked by anyone else.

2. Private Blockchain Network:

In addition, the central authority doesn’t always give each node the same rights to do things. However, because private blockchains are not open to the public, they are only partially decentralized.

Network sharing at the corporate level often requires more privacy than sharing at the individual level for data security reasons. If It is one of your wants, a private blockchain is the best choice for you to make. There is no doubt that private blockchains are a more stable network option because only a few people can see certain transactions.

People who want to use private or public blockchains have problems with them. Public blockchains can take longer to verify new data, and private blockchains are more vulnerable to fraud and bad people. It also often leads to many people relying too much on third-party management tools and favors a small group of people in the industry. A group of blockchains called a “consortium” to fix these problems.

3. Blockchain Network Of The Consortium:

It is different from private blockchains, which a single organization runs. As a result, consortium blockchains have more decentralization than private blockchains, which is more secure.

Consortiums can be hard to make because they require a lot of cooperation from many businesses. It can cause logistical problems and antitrust violations.

Some people in the supply chain may not have the technology or infrastructure to use Blockchain technology. People who do It may think that the costs of digitizing their data and connecting with other supply chain members are too high.

There is only one person in charge of the consortium blockchain, but one person is overrunning it. A person can run their rules, make changes to balances, and stop transactions that are proven to be wrong as soon as each member agrees. Aside from that, it does many other things to help businesses with the same.

There are different ways to think about when the consortium blockchain is implemented. All of the members must agree on how to communicate with each other. However, because an enterprise has less flexibility than a small business, setting up a public network that connects businesses takes a long time.

Permissioned blockchain networks use a decentralized platform, meaning data is not in a single place. Anyone can get to it at any time and from any location. It means that the whole system is safe, and your data is safe because all information exchanges and transactions are encrypted cryptographically.

4. Hybrid Blockchain:

It is the last type of blockchain we’ll talk about. These networks combine the privacy of a Permissioned blockchain with the transparency security of a public one, making them both safe and easy to use. It allows businesses to choose who has access to what data and select which information they want to make public.

Industries That Use Different Blockchain Network

Blockchain technology is suitable for many things, like the supply chain, finance, real estate, and gambling. You do not have to deal with third parties when you do business with companies or individuals.

Third-party payment providers, on the other hand, are in many ways less efficient and more challenging to use than blockchain.

As a result, energy companies, such as gas and electric suppliers and utilities, can make money from blockchain, the best technology in many ways. Another use for blockchain is to keep data safe between intelligent meters in homes.

Blockchain network protocols are also helping businesses that need efficient and secure data for ownership and management systems. Like healthcare and digital ID, find new cutting-edge solutions that are a big help. Blockchains let people stay anonymous and keep their data safe. Using public-key cryptography gives people a public key for receiving transactions and a private key for sending transactions.

Another possible benefit of blockchain for the government could be cutting costs and waste. Blockchain technology can reduce redundancies, speed up processes, and keep data safe.

How Does Blockchain Work?

There are a lot of blocks in a chain called a “blockchain.” There is a list of transactions in each block that have already happened. Because the blockchain network itself is run by computers worldwide, it keeps records. There is now a copy of the blockchain ledger on every computer, or “node,” in Its case. These nodes communicate with each other simultaneously to ensure that all the information on the chain is correct.

That means that transactions on the blockchain happen in a self-contained, peer-to-peer network. There are no borders, no one controls them, and they can’t.

When I explain how a blockchain works, there are words that you might not understand. Then don’t worry. People need to know that there are three essential parts to every blockchain: blocks, miners, and nodes.

Blocks:

Every public and private blockchain has a lot of different blocks in it. Three things make each block on the blockchain unique:

Data:

It is the information that a user sends in the block. Most of the time, the data is about money. However, there are other types of data that a blockchain can send as well, such as These things include personal health care, information about a property, contract terms, and more.

Nonce:

The nonce is a random 32-bit whole number set when the zero blocks. At This point, the hash of the block header.

Hash:

The hash is a small number that starts with zeroes and ends with a string of zeros. It goes with the nonce and has 256 bits—the soup when the first block in the blockchain. A partnership is then linked to its hash and nonce until mined. Hash is a function that helps you find things.

Ten people in one room decided to make a new currency, and they did it together. They have to keep an eye on the money flow to make sure the coins in their new money system are indisputable. When one person decides to write down everything they did, we’ll call him “Bob.” It isn’t the only person who stole money. Let’s call him “Jack.” To hide It, he changed the entries in his diary to make it look like it didn’t happen.

The secure hash algorithm, or SHA, is used in the It process. It turns the letters into a string of characters like It: There are different types of SHAs that each has different levels of complexity and serves different kinds of needs that Bob can choose from

Miners:

It’s already known that each block has a unique hash and nonce, but every block that comes after the nonce has a unique hash, too. These blocks refer to the previous block’s hash, which makes it hard to mine, especially when it comes to more prominent blockchains that are hard to mine.

A powerful computer is needed to solve the nonce and make the hash. It requires special software and tools to do It. In This case, the soup is 256 bits long, and the nonce is 32 bits long. Miners have to find the one nonce and hash combination out of the four billion possible combinations.

When a miner comes up with the right combination, block on their block list. If anyone wants to change the information in a partnership, the league itself and all the blocks that came after it must be re-mined.

Nodes:

Bitcoin nodes are found on all of the nodes in the world. That decentralization is an essential part of a blockchain platform. A chain doesn’t belong to one person or computer. Instead of having one person own the ledger, it is across the blockchain’s nodes.

With a public blockchain, checks and balances are used to keep users trusting and honest with each other. You can think of a blockchain as the ability to grow trust simultaneously as technology, which can be hard in today’s tech-driven world.

Wallets, Digital Signatures And Protocols

Wallets, digital signatures, and protocols are some things that people use to keep their money and make sure. In the same way and to guide about what Blockchain technology is?. Bob brought the ten people together (the ten people initially gathered as part of the new currency). He was vital to show them how the latest digital coins and ledgers work. It was Jack who confessed his sins to the group and said sorry. He gave Ann and Mary their money back to show how honest he was.

What is a wallet?

To explain why It could never happen again, Bob took everything into account. He decided to use a digital signature to ensure that every transaction was actual. Because everyone got their wallet, he gave them all one before that.

A wallet is a place where you keep your money here. To keep your digital money safe, you need a digital wallet, an online platform, or an exchange or platform to store it. Some assets can be sent to public wallet addresses, strings of letters that need to be sent. You need to know the public key used to get the address of each wallet.

Digital signature

Every person you need to know about Bitcoin Wallets for Beginners: Everything you need to know about Bitcoin wallets for beginners: A digital signature is a way to make sure that when you want to make a payment, you need two things: a wallet, which is an address, and a private key.

The private key is a string of numbers that are not the same. It is not the case with the address. The private key must be kept confidential. A private key controls the money in a wallet linked to it.

A cryptographic key is a long string of numbers and letters to break codes. It is used to make cryptographic keys. Key generators, or keygens, are used to make them. These keygens use very complicated math that includes prime numbers to make keys. To encrypt or break information, you can use keys like It to do it.

Protocols

Blockchain technology has a lot of rules that are written into it. These rules are called “protocols.” Protocols are the names of those rules. The use of specific protocols makes the blockchain what it is: a distributed, peer-to-peer, and secure information database. Because the network is entirely self-governed and not controlled by anyone, blockchain protocols ensure it runs the way its creators planned.

The difficulty of mining is changed every 2,016 blocks. Mining difficulty, in a way, balances the network to account for how many miners there are. Some blocks become harder to get to when there are a lot of miners. Fewer miners make it easier to mine blocks, making it more appealing for other miners to join in.

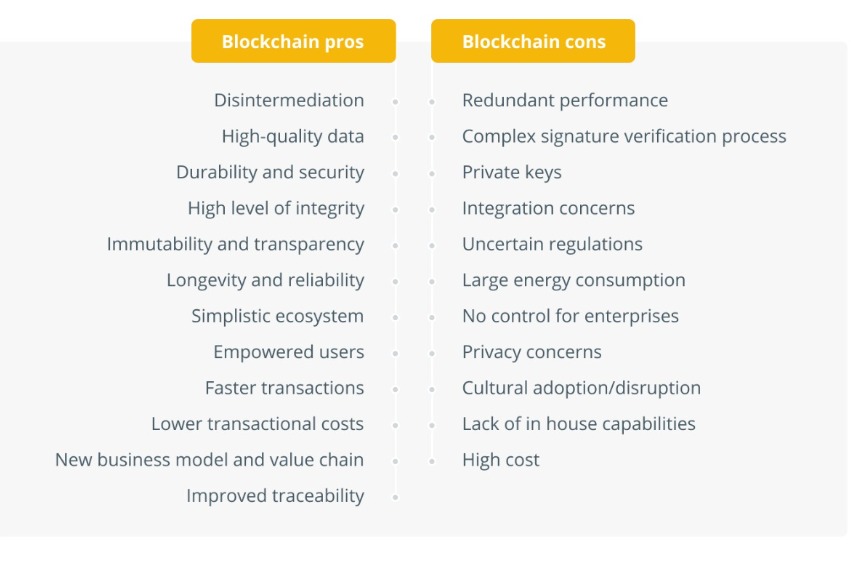

Blockchain Technology: Pros And Cons

A look at some of the good and bad things about blockchain technology: most blockchains are built with a decentralized database that acts as a distributed ledger. Also, it is how most of them are made. So, it keeps track of and stores data in blocks linked together by cryptographic proofs. These blockchain ledgers store and track data in chronological order, and these proofs connect unions.

Blockchain has had a significant impact on technology day by day—also, on many businesses, including better security in situations where people don’t trust each other. However, the fact that it isn’t centralized has a lot of downsides. For example, blockchains aren’t as efficient as databases usually run by a single person. They also take up more space.

What Is Decentralization In Blockchain, And Why Is It Important?

Blockchains are a type of distributed database. If you’re on a ” blockchain chain,” you can see everything on that chain. There is no single node or computer here that controls the information it holds. Every node in the blockchain, what is Blockchain technology? It is all done without having one or more people in charge of everything.

It is essential because no single point of failure could bring down the blockchain, making it a necessary part of blockchain systems. Also, the nodes of a blockchain are logically centralized because the whole thing is a network that does certain things.

Transparency Of Blockchain Network

People who use blockchain technology need to be more open about what they do. Anyone who looks at the blockchain can see every transaction and its hash value. People who use the blockchain can act anonymously if they want, or they can give out their identity to other people if they want. The only thing seen on the blockchain is a record of transactions between wallets.

It’s impossible to change the record of a transaction on the blockchain after it’s been recorded. Why? That transaction record is linked to the history of every previous one, making it impossible to change. Documents on the blockchain last for a long time. They’re organized by date in chronological order, and other nodes can see them.

However, it would be hard to use blockchain technology as a standard database. Is there a way to store three gigabytes of files on the blockchain in the same way you would keep them in databases like Microsoft Access or FileMaker? It would be wrong. Most blockchains don’t work well for It, either because they aren’t built for it, or they don’t have enough space.

How Secure Is Blockchain Technology?

Even though the blockchain can be hacked, its decentralized nature makes it more secure. A hacker or criminal would need to have control of more than half of the machines in a distributed ledger to change it, so they would need to be very powerful.

Blockchain networks like Bitcoin and Ethereum (ETH) are open to anyone with a computer and an internet connection. It means that anyone can use these networks. It’s more likely that having more people on a blockchain network will make the web more secure than making it less safe. More nodes participate, which means more people review each other’s work and report bad people.

It can be challenging for people to join private blockchain networks that require an invitation from someone else. That’s one reason why It isn’t always the case, though. In addition, blockchain can help stop “double-spending” attacks in payments and money transfers.

Cryptocurrency attacks are a significant source of worry. In a double-spending attack, a person will spend their cryptocurrency more than once, so they will lose money. It’s not a problem when you deal with cash. There is no more money to spend if you spend $3 on a cup of coffee. As for crypto, there’s a chance that someone will pay the crypto many times before anyone notices.

Here, blockchain can help. In a cryptocurrency’s blockchain, everyone on the network must agree on the transaction sequence, confirm the most recent transaction, and make it public, which helps keep the network safe.

Where Can Blockchain Technology be Used?

The last part of The article will talk about some of the many ways that a blockchain. A type of “smart contract” can with the help of a technology called a blockchain.

Smart contracts are similar to traditional arrangements in that they set out the rules and penalties for a specific agreement. However, the big difference is that intelligent contracts automatically follow through on their promises. Because of how they are written, innovative arrangements only work if certain conditions are met.

Decentralized Finance

Decentralized finance, or Defi, uses blockchain technology that allows people to have the same features as people in the mainstream financial world but is more decentralized. Using a variety of defi solutions, people can borrow and lend money and access other opportunities that a single individual or group does not control.

Non-fungible Tokens

Non-Fungible tokens, or NFTs, are a type of blockchain technology in many different ways. Such tokens can be proven unique and can’t be traded one-for-one with other tokens for the same value. One possible use case for NFTs is the authentication of art, with art pieces linked to NFTs that can show that they are accurate and belong to the rightful owner.

Supply Chain

A supply chain that uses blockchain technology can help people prove the origins of things like ingredients and food. Also, It can also help people learn about a given supply chain.

Warranty Claims

When warranty claims have to be settled, they can be very costly, time-consuming, and difficult for the people who want to make them. Also, it is possible to use blockchain technology to create smart contracts, which will make the process a lot easier.

Insurance Claims

With smart contracts, rules for certain insurance-related situations are set up. It’s possible that with the help of blockchain technology, you could submit your insurance claim online and get an automatic payout right away if your claim meets all the rules.

Identity Verification

However, with the help of blockchain and its decentralization, people could prove their identities online much faster and, in some cases, more safely. With the use of the blockchain, keeping online identity data in one place could become a thing of the past. It means computer hackers would no longer have centralized points of vulnerability to attack.

The Internet things that (IoT)

These things have certain technical specifications that make Them possible.

Blockchain technology could play a role in the future of IoT because it protects against hackers. In this case, because the blockchain is built for decentralized control, it should be able to handle the growth of IoT.

Archive and store their files:

Google Drive, Dropbox, and other companies have made it easier to keep documents in the cloud using centralized methods. Hackers are drawn to sites that are all in one place. Blockchain and its smart contracts can help a lot with It.

MFighting Crime

It could help fight money laundering if the technology gets more attention. Blockchain and smart contracts could help.

Blockchain allows for a more in-depth look at the system instead of keeping an eye on where people come and go. As blockchain is a decentralized network in which each user or node is in charge of verifying updates, it makes the web more secure.

Voting

Smart contracts and the blockchain could improve voting in elections and other processes. Over time, there have been a lot of applications that are similar to each other.

The Feature Of Blockchain Technology

Recently, we have seen a lot of progress in blockchain technology. We’re closer to a decentralized, trustless internet, transaction transparency, etc.

They will help us deal with these new social issues and redefine what wealth means in the brave new world of digital money.

Even though blockchain technology has already shown its worth in almost every field, it looks like the best is still to come.

However, blockchain technology goes in the future, especially when it comes to banking services, money transfers, decentralized markets, and other things, as well as when it comes to blockchain.

Conclusion

Finally, blockchain technology is becoming more and more popular and getting a lot of support from businesses. Each type of blockchain could improve trust and transparency and better record transactions.